By Asefon Abdulganeey Stephen

Drawing from historical data and policy developments, tracing the trajectory from the 1972 Students Loan Board to the present-day Nigerian Education Loan Fund (NELFUND), highlighting patterns of weak implementation, poor recovery, and governance gaps. Asefon Abdulganeey Stephen examines the origins, evolution, and recurring challenges of Nigeria’s student loan system, with the aim of interrogating whether the current framework can deliver equitable access to higher education without repeating past failures.

Higher education has always been one of the surest paths to success. Yet in the 1960s, Nigerian students only stood at the beautiful gates of universities with pockets swollen with emptiness but a heart filled with dreams and ambitions. And when the cost of education becomes so uneasy, what happens to those dreams and ambitions? What then remains of the hopes of the less privileged?

At the dawn of independence in 1960, Nigeria’s university system was still in its infant status. Only a handful of universities existed and a concomitant small number of students. According to A. Babatunde Fafunwa’s The Growth And Development of Nigerian Universities, roughly 1,395 students were enrolled across all Nigerian universities in 1960.

However, in 1968, there had been a serious preponderance in the number of enrolled students. The number of students, from 1,395 students in 1960, rose increasingly to 8,617 at the beginning of 1968, with the University of Ibadan holding 3,117 students, Ahmadu Bello University 1,745, Unilag 2,094, and Ife adding to the statistics with 1,661 students. (Provided by Professor Archibald Calloway; calculations based on information provided by the Nigerian Universities Commission). The statistical records for the other institutions are currently unavailable.

In the 1970s, the preponderance of enrolled students seemed a paradox as it posed greater challenges to the government. More students unequivocally required more classrooms, more facilities, and more lecturers. All these became a conundrum to the then Nigerian government, which was still battling with a wave of economic and social instabilities: the relics of the Nigerian Civil War and just 10 years from the shackles of colonization.

Also, aside from the overwhelming increase in the numAber of students, a wave of agitation had been staged in various universities as the end-of-session examination fee crisis broke out. Nigerian students, who hadn’t paid their tuition fee, cried out to the federal government to allow them to take their end-of-session exam. As noted in a speech made by past pro-chancellor and chairman of the governing council of Ambrose Alli University published on Vanguard, the protest continued in the University of Lagos, University of Ibadan, and University of Benin. The students were on vacation after they had been allowed to write their exam when they heard that the federal government had promulgated the establishment of the Nigeria Student Loan Board with its headquarters in Lagos. A session loan was between #300 and #500 depending on the years of the program.

Understanding the popular mantra “necessity is the mother of invention,” the Nigerian government sought ways to help all Nigerian students to have equitable access to higher education. And the steps toward making education accessible to all students birthed the first Students Loan Board when the military government under Gen. Yakubu Gowon promulgated Decree No. 25 in 1972.

The cardinal criterion for the loan was financial need. Nigerian students who came from a poor or less-privileged background were eligible to receive the loan. Students, who were already on scholarships and bursaries, were excluded from applying for the loan. While there is no source that withholds the due time for repayment, Vanguard’s publication, “ASUU Strike: A return to students loan board of 1974,” published on the 25th of September 2022, reveals that the loan was 20 years repayable.

Unfortunately, the student loan scheme began to become a shadow of its former self in the late 20th century owing to poor repayment. 1991 witnessed the dimming light of the loan scheme as only about #6,000,000.00 (13%) had been recovered out of the overall #46,000,000.00. Also, legal loopholes and administrative weaknesses had been said to have a major determinant too. The 1972 loan scheme had no provision for legal actions to compel, if student debtors refused or failed to pay. Though their repayment of the loan 2 years ago reflects their sincerity and honesty, the long time of 45 years, which the 1970s students took to repay the loan, underpins the aforementioned challenges.

Guided by the principles of “if at first you don’t succeed, try, try again,” the Nigerian government under military rule in 1993 replaced the 1972 Student Loan with the Nigeria Education Bank with the Decree No. 50. Hoping it would water the soil where the former failed to. However, in its nature and creation, the Nigeria Education Bank was slightly different from the 1972 one. Nigeria Education Bank was designed as a revolving bank for broader educational funding.

In the question of effectiveness, evidence claims that EDUBANK had become a somewhat failed project, as it never became operational from nearly its inception. Also, there was no governing board that could administer efficacious control over the scheme, the minister of education, hence, acted in its place—an action that was against the legal framework and declined proper governance. In response to its inactivity, a ministerial committee was set up to discuss its closure in 2001. To a very large extent, it is accurate to assert that the 1972 student Loan board and 1993 Nigeria Education Bank were partially failures due to administrative shortcomings.

After the closure of the Nigerian Education Bank in 2001, the question of making education equitable to all never remained a silent breath between 2001 and 2024. The attempt, to create another student loan scheme largely remained on paper or non-existent.

Would the closure of EDUBANK be the end of the government’s intervention into seeking and establishing equitable access to higher education? This question remained fallow for roughly two decades. However, just as the rising cost of education alongside the immense desire to make education accessible to all, in 2019, Femi Gbajabiamila, a speaker of the House of Representatives, sponsored the Student Loan Bill, giving hope to students with poor backgrounds.

The bill was signed into law on the 3rd of April, 2024 by the elected president, Bola Ahmed Tinubu.Under this new legislation, student loan schemes would function through a new corporate body called Nigerian Education Loan Fund[NELFUND]. In his speech, the president proclaimed that the student loan law was a testament to the Nigerian government’s commitment to Education as a tool to “fight poverty effectively”. On the 24th, May, Student loan had become operational, and by the 10th of July, it had been extended to state-owned tertiary institutions.

Against this backdrop,it is noteworthy that on the 29th of May, 2023 while delivering his inaugural speech at Eagle square in Abuja, President Bola Ahmed Tinubu announced the removal of subsidy, stating that the government had no provision for subsidy. This development signaled critical conditions for Nigerians who seemed to have been entrapped between hell and Serpents; the student loan and fuel subsidy removal. One then is compelled to raise two posers; Is making the leaders of tomorrow bunch of debtors today the perfect way to make higher education equally accessible, or simultaneous removal of subsidy alongside student loans the only approach for a nation to fight poverty effectively?

Regardless of personal opinion towards these posers, the Nigerian government had put to us an unequivocal “YES” answer.

The Nigerian government seemed to have offered what one can pronounce “evil assistance”. Put differently, while the removal of subsidies posed and continues to effectuate rising cost of living, Student loan becomes an instantaneous antidote, but one that would add insult to injury in the future.

That said, the Nigerian government could do better by not making debtors out of Nigerian students but embarking on a policy that would foster national development and economic stability.

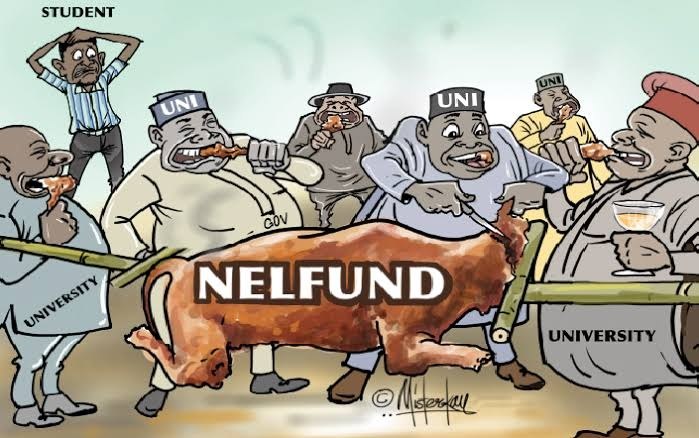

NELFUND and the Familiar Shadow of Institutional Failure

Beyond policy documents and government assurances, a more critical conversation is beginning to take shape around NELFUND, and it is one rooted in experience, not speculation.

In an opinion piece published by Leadership Newspaper, titled “NELFUND: Against A Culture of Impunity,” Dakuku Peterside offers a perspective that resonates strongly with the concerns of many Nigerian students.

We acknowledge what many students already know: NELFUND, on paper, is exactly what the system has long needed. An interest-free loan, digitally managed, with minimal human interference, it sounds like a clean break from the inefficiencies and gatekeeping that have historically defined access to educational funding in Nigeria.

For students who have had to defer dreams, depend on extended family, or hustle through school just to stay enrolled, the idea of NELFUND is more than policy, it is relief.

But it should be carefully pointed out that Nigeria has a way of turning good ideas into cautionary tales.

The early murmurs of irregularities, allegations of unauthorized deductions, and fears of fund diversion may seem premature, but they are not surprising. In a system where public trust has been repeatedly eroded, Nigerians do not wait for official confirmation before becoming skeptical. The default expectation, shaped by history, is that somewhere along the line, something will go wrong.

Nigeria’s earlier student loan interventions followed a similar trajectory of strong intentions and weak implementation. The 1972 Student Loan Board and the Nigeria Education Bank of 1993 both struggled under administrative inefficiencies, poor recovery structures, and governance lapses, eventually fading into irrelevance. What failed was not the idea of student loans but the system built to sustain them.

Without strong accountability mechanisms, even digitally driven systems can be compromised. Funds can be rerouted, processes quietly altered, and oversight weakened, all without immediate visibility.

If NELFUND fails, it will not merely be another government initiative that falls short of expectations. It will disrupt academic pursuits, widen existing inequalities, and leave yet another generation struggling to cope with higher education under persistent financial strain. In effect, access to education, already precarious, will become even more restricted.

And for many students watching closely, the question is no longer what NELFUND is designed to do, but whether it will be allowed to work.

Cover image credit: Leadership Newspaper

Story originally published by ZIK press